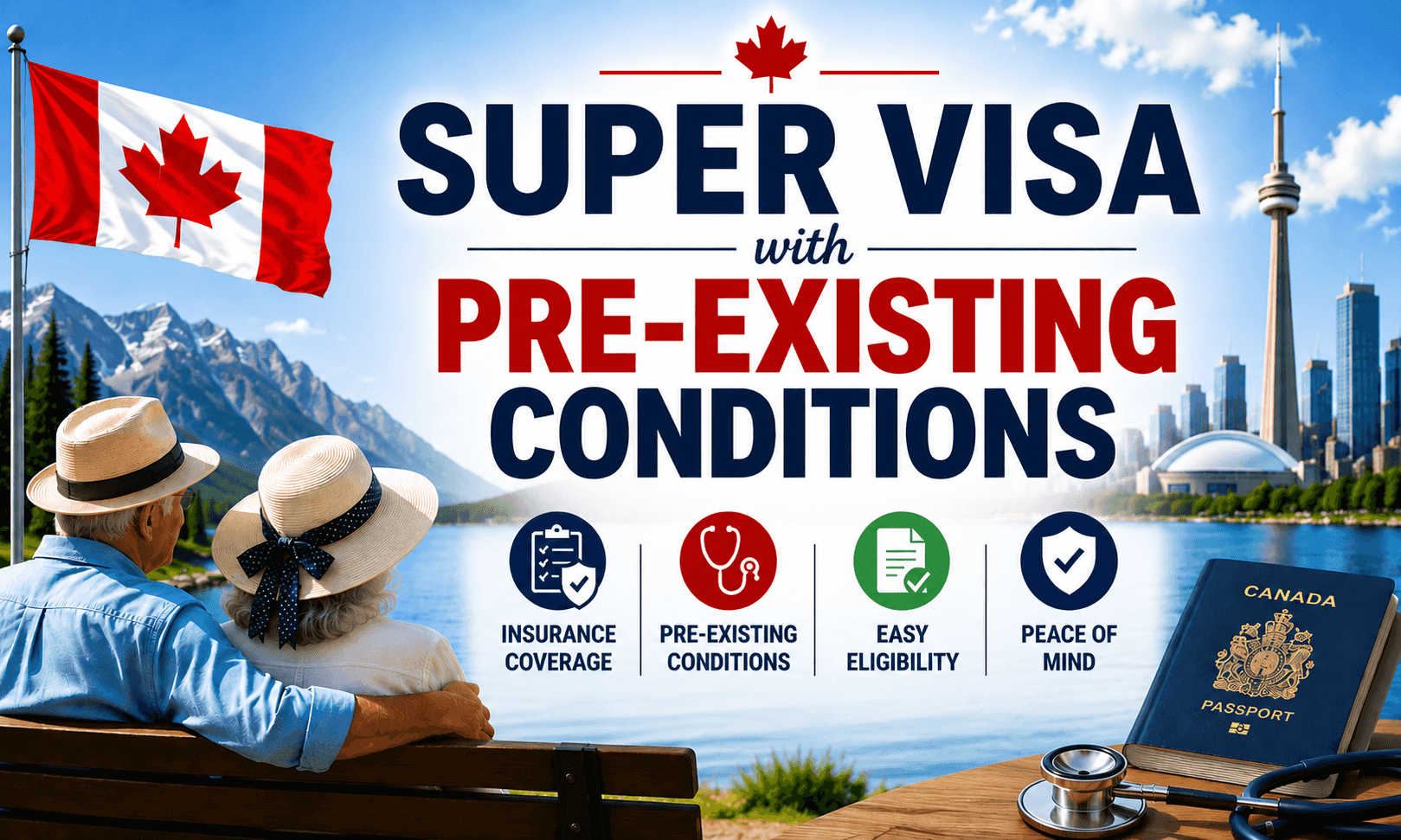

Super Visa Pre-Existing Conditions 2026: Manulife vs GMS vs 21st Century Coverage Compared

If your visiting parent or grandparent has high blood pressure, diabetes, a previous heart event, or any other ongoing condition, the Super Visa insurance question changes from "How cheap can I get?" to "Which insurer will actually cover me if something happens?"

This guide compares how the five Canadian insurers featured on DaddySafe Super Visa handle pre-existing conditions in 2026.

Manulife, GMS, 21st Century, Destination Canada, and the RIMI Standard Plan, so you can buy with confidence and avoid the most common claim denial trap.

What "stability period" actually means

Every Canadian Super Visa insurer pays for medical emergencies caused by a condition only if that condition has been "stable" for a defined number of days before the policy start date. "Stable" generally means:

No new diagnosis

No new symptoms or worsening symptoms

No new medications, dose changes, or stoppages

No new tests, hospitalizations, or specialist consultations

If the condition has been stable for the required number of days, it is automatically covered (or covered via a small rider). If not, the insurer will deny that specific claim. This is the single biggest reason Super Visa claims get refused and the reason picking the right insurer matters.

Stability periods at a glance 2026

Manulife CoverMe Travel for Visitors to Canada stability periods of 90 / 180 days depending on age and rider chosen. Often the most generous on cardiac and pulmonary conditions.

GMS Immigrants & Visitors to Canada 90, 180, or 365 day options. Strongest for predictable diabetes and hypertension cases at competitive premiums.

21st Century Travel Insurance flexible 90 / 180 day stability with the most aggressive deductible options to lower premium.

Destination Canada Travel Insurance built-in standard stability provisions; strong value for ages 70+ with stable conditions.

RIMI Standard Plan clean and predictable stability rules; often a good middle-ground choice.

Get a personalized quote and we'll match you to the insurer with the right stability rule for your parent's situation.

How each insurer treats the most common conditions

1. High blood pressure (hypertension)

The most common pre-existing condition we see for Super Visa applicants. GMS and Manulife usually win here both offer 90-day stability if blood pressure is well-controlled on stable medication. 21st Century is competitive for ages 60–69 with a higher deductible.

2. Type 2 diabetes

GMS often comes in cheapest for diabetic applicants under 75 if no medication change in the last 6 months. Manulife is the safer choice if the diabetes is more complex (insulin-dependent, with complications). The RIMI Standard Plan is a strong middle pick.

3. Previous heart event (heart attack, stent, bypass)

This is where insurer choice matters most. Manulife typically has the broadest coverage for stable cardiac history if the event was more than 12 months ago and there have been no symptoms or interventions since. Destination Canada can also work well for ages 70+ with stable cardiac history.

4. Cancer history

Most insurers require the cancer to be in full remission with no treatment for a defined period. Manulife tends to have the clearest remission rules. Always disclose, always document.

5. Stroke / TIA history

Toughest category. Manulife and GMS are usually the only realistic options if the event was more than 12 months ago and the parent has been stable since.

The 3 mistakes that get pre-existing claims denied

Not disclosing. Skipping a condition on the medical questionnaire voids the policy entirely for every condition, not just the undisclosed one.

Buying a "no medical questions" plan. These plans almost always exclude pre-existing conditions completely. Cheaper upfront, useless when it matters.

A medication change just before travel. Even a tiny dosage adjustment 30 days before the start date can break the stability period. Coordinate with the parent's doctor before locking in the policy.

How to choose the right insurer for your parent

The fastest answer is to run a quote on DaddySafe. Our system asks the medical questions and only shows you the plans that will actually cover the disclosed conditions so you don't waste time pricing plans your parent will never qualify for.

Cheapest pre-existing approved plans in 2026

Real ranges we typically see for stable, well-managed conditions, $100,000 coverage, $0 deductible:

Age 60–64: $1,650–$2,300/year (GMS or Manulife usually cheapest)

Age 65–69: $2,000–$3,000/year (GMS, Manulife, or 21st Century)

Age 70–74: $2,800–$4,200/year (Manulife or Destination Canada)

Age 75–79: $4,000–$6,000/year (Manulife or RIMI Standard Plan)

Age 80+: $5,800–$9,500/year (Manulife typically the only option for complex history)

Premiums fall sharply with a $1,000 deductible, often 15–25%.

Buy with confidence

Whether your parent is healthy, mildly hypertensive, diabetic, or has a more complex history, there is a Canadian Super Visa insurer that will cover them properly. The trick is matching the right insurer to the right condition, which is what DaddySafe is built for.

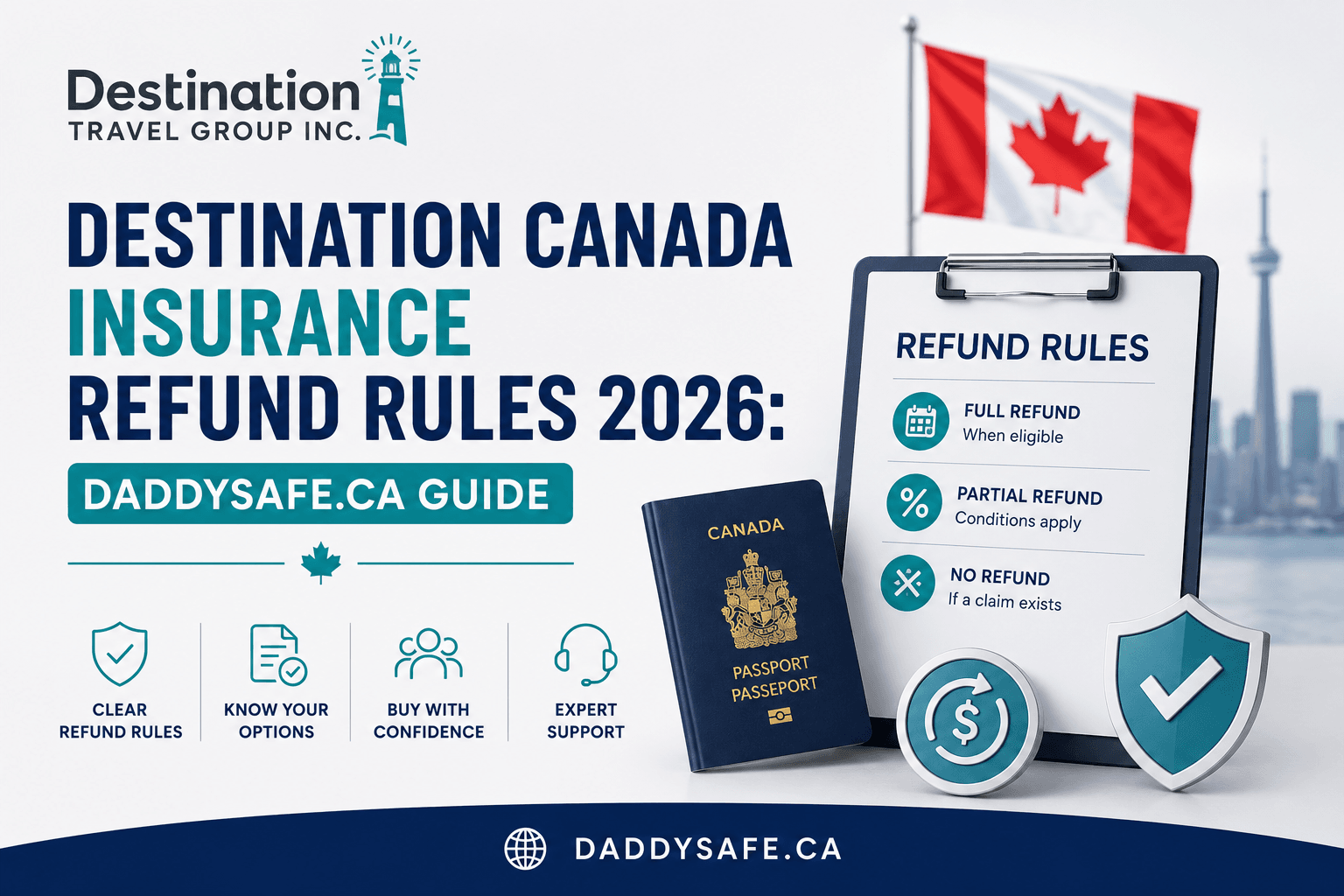

Compare Manulife, GMS, 21st Century, Destination Canada & RIMI Super Visa insurance now instant quote, IRCC-compliant letter, full refund if the visa is refused.

Related reading on DaddySafe: Super Visa Insurance Cost in Canada 2026: Cheapest Plans & Real Quotes | How to Buy Super Visa Insurance in Canada in Under 5 Minutes | Super Visa Income Requirements 2026: LICO, Sponsor Rules & Insurance Proof | Visitor Insurance with Pre-Existing Conditions: 2026 Coverage Guide

Related Blogs