Cheap Visitor Insurance for Canada: How to Get the Best Price in 2026

If you are looking for cheap visitor insurance for Canada, you are not alone. Premiums add up fast, especially for older visitors or longer stays – and a lot of people end up overpaying simply because they buy from the first website they land on. The good news is you can get strong, reliable coverage at a much lower price if you know how to shop. This guide shows you exactly how to find cheap visitor insurance in Canada in 2026 – without giving up the protection that actually matters.

What “Cheap” Visitor Insurance Really Means

Cheap does not mean weak. The cheapest plan on the market is not always the lowest premium – it is the plan that gives you the best value per dollar. A $1.50 per day plan with $10,000 coverage and a $1,000 deductible is not actually cheap if a single hospital visit blows past the limit. Real value means the right coverage at the lowest fair price for your visitor’s age, trip length, and health.

Why Visitor Insurance Premiums Vary So Much

Two travelers with the exact same trip can pay very different premiums depending on a handful of factors. Understanding these factors is the first step to finding cheap visitors to Canada insurance that still delivers real protection.

Age of the visitor – the single biggest cost driver. Premiums climb sharply after age 60.

Length of stay – longer trips cost more in total, but per-day rates often drop.

Coverage amount – $25,000, $50,000, $100,000, or higher.

Deductible – the amount you pay out of pocket before the insurer steps in.

Pre-existing conditions – plans with stable condition coverage cost slightly more.

Insurer – different Canadian insurers price the same coverage very differently.

7 Smart Ways to Find Cheap Visitor Insurance in Canada

1. Compare Multiple Insurers Side by Side

Buying directly from one insurer means paying retail. Compare quotes from at least four or five top Canadian insurers in one place to spot the best price. A 60-second comparison can easily save you 20 to 40 percent on the same level of coverage. See our complete guide on how to compare visitor insurance plans for the exact factors that matter.

2. Choose a Higher Deductible

Bumping your deductible from $0 to $250 or $500 can drop your premium noticeably without changing your overall protection. If your visitor is young and healthy, this is one of the easiest ways to lower the price.

3. Match Coverage to the Trip – Do Not Over-Insure

A two-week tourist trip does not need the same coverage as a one-year stay. Pick a coverage amount that fits the visitor’s age, health, and trip length. $100,000 is a solid baseline for older visitors. Younger, short-trip travelers can often get away with less.

4. Buy Early

Some insurers offer better rates when policies are bought a few weeks in advance. Last-minute purchases are not always more expensive, but planning ahead gives you more pricing options.

5. Skip the Add-Ons You Do Not Need

Trip interruption coverage, accidental death riders, and other extras add up. If your visitor only needs medical protection, skip the bells and whistles and put the savings toward higher emergency medical limits instead.

6. Pay Annually Instead of Monthly

For longer policies, paying upfront often unlocks a small discount and avoids monthly admin fees. If cash flow allows, this is a quiet way to save.

7. Look at Family or Group Quotes

If you are insuring two parents at the same time, ask for a couple or family quote. Some insurers offer combined discounts that beat two single policies.

Don’t Sacrifice These – Even When Going Cheap

Cheap is smart. Cheap with gaps is not. No matter how aggressively you shop, do not give up these basics:

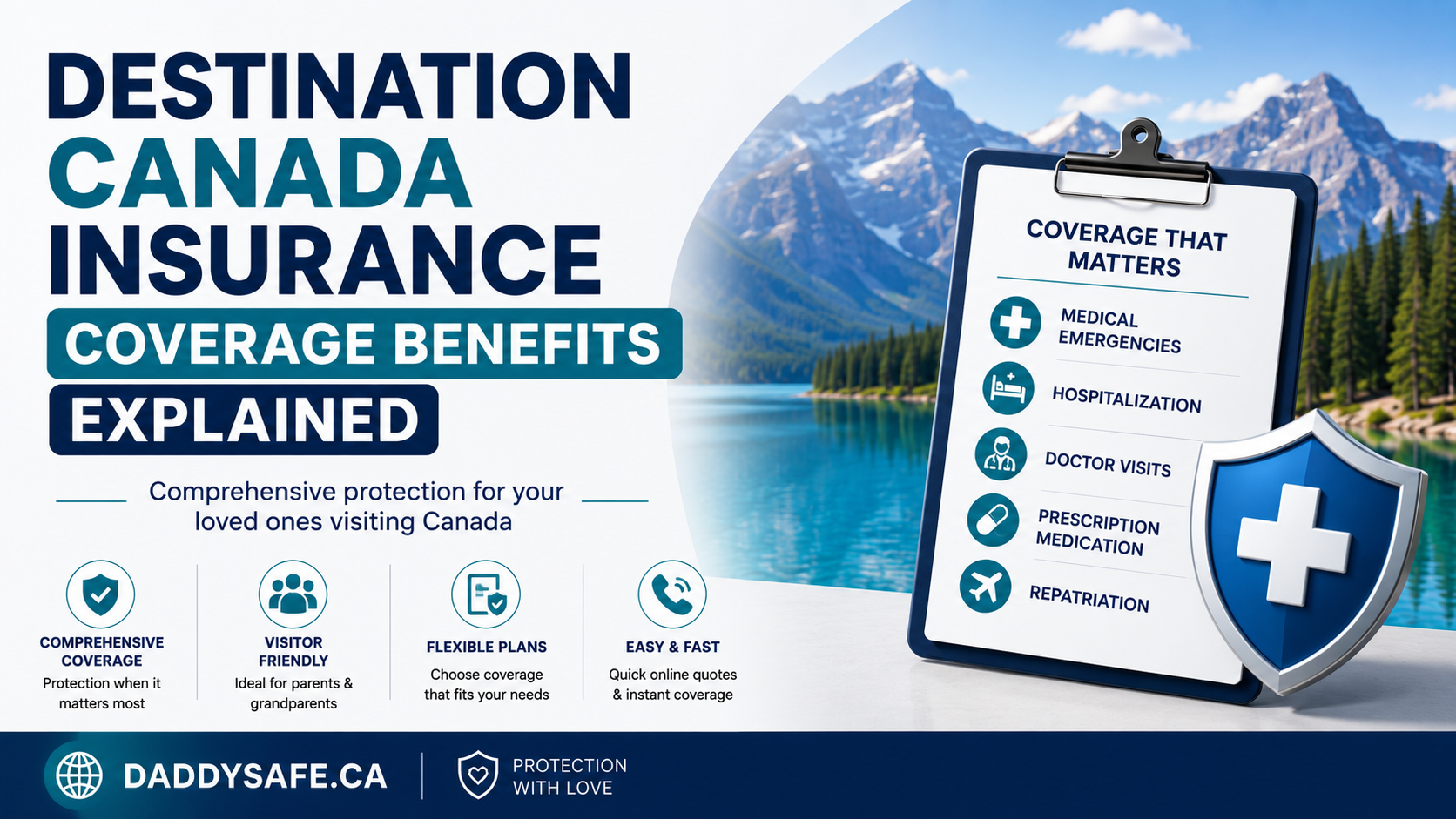

Minimum $100,000 coverage for older visitors and longer stays

24/7 emergency assistance with a real Canadian phone line

Pre-existing condition coverage if your visitor takes any regular medication

Clear claims process with reasonable documentation requirements

Refund policy in case the visa is denied or the trip is cancelled before the start date

For a deeper look at exactly what should be included, see our breakdown of emergency medical insurance for visitors to Canada.

Common Mistakes Cheap Shoppers Make

Choosing $25,000 coverage to save a few dollars – then facing a $40,000 hospital bill

Skipping the pre-existing condition rider when the visitor takes regular medication

Buying from a foreign insurer instead of a Canadian one (a problem if the visitor is on a Super Visa)

Falling for fake comparison sites that only show one or two providers

Buying after the visitor has already arrived in Canada

Real Price Examples for 2026

Actual premiums change with age, length of stay, deductible, and insurer, but here is a rough idea of what cheap visitor insurance for Canada looks like in 2026:

Age 30, 1-month trip, $100,000 coverage: roughly $50 to $80 total

Age 50, 3-month trip, $100,000 coverage: roughly $250 to $400

Age 65, 1-year trip, $100,000 coverage: roughly $1,500 to $2,500

Age 75, 1-year trip, $100,000 coverage: roughly $2,800 to $4,500

Comparing online is the only way to know the real price for your specific visitor.

Cheap Super Visa Insurance: A Special Note

If your visitor is applying for a Super Visa, the cheap-shopping rules change slightly. You still want the lowest fair price – but the policy must meet IRCC requirements (minimum $100,000 coverage, valid one year, issued by a Canadian insurer). Cheap plans that do not meet these rules will get a Super Visa application refused. See our explainer on visitor insurance vs Super Visa insurance to make sure you are buying the right product.

Why Comparing Online Beats Buying Direct

Online comparison platforms like DaddySafe pull live quotes from multiple top Canadian insurers in seconds. You see prices, plan highlights, and exclusions in one view. There is no commission bias, no pressure, and no need to fill the same form on five different websites. For most buyers, that is the difference between paying retail and getting the genuinely cheapest plan that still protects what matters.

Conclusion

Cheap visitor insurance for Canada is absolutely possible in 2026 – you just need to shop smart, not random. Compare multiple insurers, pick the right deductible, match coverage to the trip, and skip the add-ons you do not need. Get an instant visitor insurance quote in 60 seconds, compare the best Canadian providers in one place, and lock in real coverage at the lowest fair price.

Related Blogs