Super Visa Insurance Cost in Canada 2026: What You'll Actually Pay

Let me be straight with you.

When a family calls me and asks "how much does Super Visa insurance cost?" - there's no single answer I can give them in 10 seconds. And anyone who gives you one without asking a few questions first is guessing.

The cost depends on your parent's age, their health history, which provider you go with, and how much risk you're comfortable carrying yourself through a deductible. Get those four things right and you could save over $1,000 a year compared to just picking the first plan you find on Google.

I've helped hundreds of families across Canada navigate this. Here's exactly what I've seen - with real numbers from actual provider rate cards.

What the Government Actually Requires

Before we get into pricing, here's the non-negotiable part.

IRCC requires every Super Visa applicant to have:

Minimum $100,000 CAD in emergency medical coverage

A policy from a Canadian insurance company - not a foreign one

Coverage valid for at least one year from the date they land

The policy must cover health care, hospitalization, and repatriation

That's the floor. Some families go higher - $150,000 or $200,000 - especially if their parent is older or has health conditions. Whether that's worth it depends on the situation.

Four Things That Actually Move the Price

I see families get surprised by their quote all the time. Usually it comes down to one of these four things.

Age: This is the biggest one. A 55-year-old parent and a 72-year-old parent are not paying the same premium - not even close. Insurers price based on medical risk, and the numbers jump significantly once you cross 70.

Pre-existing conditions: Does your parent have diabetes? High blood pressure? A history of heart issues? If yes, you need a plan that actually covers those conditions. Standard plans exclude them entirely. Enhanced plans cover them - but cost more. Skipping the enhanced plan to save money and then having a $90,000 uncovered cardiac event is not a trade-off worth making.

Deductible: This one is underused. Choosing a $500 deductible instead of $0 typically saves 15% off your premium. For a $2,400/year policy that's $360 back in your pocket - every year. If your parent is healthy and unlikely to make a claim, this is an easy decision.

Monthly vs. annual payment: Most people don't realize they can pay monthly. It's available from several providers for $100,000 coverage on policies of 180 days or more. There's a small surcharge but for families managing cash flow, spreading $2,000 over 12 months at around $170/month is a lot more manageable.

Compare live quotes for your parent's specific situation at DaddySafe.ca →

Real Numbers: What Each Provider Charges in 2026

The table below is built from actual rate cards - not estimates, not ranges pulled from thin air. These are the daily rates and annual premiums for a parent aged 65-69, $100,000 coverage, $0 deductible, 365-day policy.

All figures in Canadian dollars. Rates sourced from current provider rate cards and are subject to change. Always get a live quote at DaddySafe.ca before purchasing.

Provider | Plan Type | Pre-Existing Covered | Daily Rate | Annual Premium |

|---|---|---|---|---|

RIMI Standard — Plan 1 | Standard | ❌ No | $4.44 | ~$1,621 |

RIMI Enhanced — Plan 1 | Enhanced | ✅ Yes (stable 180 days) | $5.05 | ~$1,843 |

Destination Canada — Option 2 | No Pre-ex | ❌ No | $5.70 | ~$2,081 |

21st Century Standard | Standard | ❌ No | $6.53 | ~$2,383 |

GMS Visitors to Canada | Standard | ✅ Stable (waived before arrival) | $6.59 | ~$2,405 |

Manulife — Plan A | Standard | ❌ No | $6.82 | ~$2,489 |

Destination Canada — Option 1 | With Pre-ex | ✅ Yes (stable per age) | $7.19 | ~$2,624 |

Manulife — Plan B | Enhanced | ✅ Yes (stable 180 days) | $7.50 | ~$2,738 |

21st Century Enhanced | Enhanced | ✅ Yes (stable 180 days) | $8.93 | ~$3,259 |

The spread here is significant. Over $1,600 difference between the cheapest and most expensive option - for the same age, same coverage amount. That's real money.

But here's the thing. RIMI Standard at $1,621/year is only the right choice if your parent is in good health with nothing pre-existing to worry about. The moment there's a health condition in the picture, you need to move up. And in that case, RIMI Enhanced at $1,843/year gives you pre-existing condition coverage for just $222 more per year. That's less than $20 a month for protection that could cover tens of thousands in hospital costs.

How Much More Do You Pay As Age Increases?

I want to show you something that doesn't get talked about enough.

Using Manulife Plan A as a consistent reference point, here's how the annual premium climbs as your parent gets older - same $100,000 coverage, same standard plan:

Age Group | Daily Rate | Annual Premium |

|---|---|---|

40–54 | $4.76 | ~$1,737 |

55–59 | $5.14 | ~$1,876 |

60–64 | $6.00 | ~$2,190 |

65–69 | $6.82 | ~$2,489 |

70–74 | $9.92 | ~$3,621 |

75–79 | $12.87 | ~$4,698 |

See that jump between 65-69 and 70-74? That's over $1,100 more per year - same plan, same coverage, just five years older.

This is why I always tell families: don't delay this application thinking you'll get to it later. Every birthday that moves your parent into the next bracket costs you real money, year after year.

**The Pre-Existing Condition Question **- This Is Where Most Families Get It Wrong

I'm going to be direct about this because I've seen it go badly.

A standard plan that excludes pre-existing conditions is not "good enough" for a parent who takes blood pressure medication, manages Type 2 diabetes, or had a cardiac procedure three years ago. If something happens and the claim is related to that condition - the insurer can and will deny it. You'll be left with a bill that could easily run into six figures in a Canadian hospital.

Here's how the stability periods work across providers. Your parent's condition must be "stable" - meaning no change in treatment, medication, or symptoms - for the following periods before the policy starts:

Destination Canada: 90 days stable (age 59 and under) · 120 days (age 60-69) · 180 days (age 70-79)

Manulife : 180 days stable for all ages

21st Century Enhanced: 180 days stable for age 55+ · No medical declaration needed under 55

GMS: Waiting period waived entirely if purchased before arrival or replacing existing Canadian coverage with no gap in coverage

If your parent has a condition that has been managed and stable for the required period - get the enhanced plan. The extra cost is modest. The protection is not.

The Deductible Strategy Most Families Don't Use

Here's a quick way to reduce your premium that almost nobody talks about.

Every major provider lets you choose your deductible - the amount you agree to pay yourself before the insurance kicks in. The savings are real:

Deductible | Saving Off Base Premium |

|---|---|

$0 | No discount |

$100 | ~5% off |

$500 | ~15% off |

$1,000 | ~20% off |

$2,500 | ~25–30% off |

$5,000 | ~35% off |

$10,000 | ~40% off |

On a $2,400 annual premium, choosing a $500 deductible saves you roughly $360 per year. Over a two-year Super Visa stay that's $720 back.

My suggestion for healthy parents who have no active medical concerns - take the $500 or $1,000 deductible. Keep the savings. Use them for something better.

For parents with health conditions who are more likely to need care - stick with $0 or $100. Don't add financial stress on top of a health event.

Can You Pay Monthly? Yes - And Here's How

One of the most common things I hear is: "We want to do this but we don't have $2,000 sitting around right now."

Fair. Monthly payment plans exist.

Destination Canada offers monthly payments for policies with a minimum $50,000 aggregate limit and at least 180 days of coverage.

RIMI offers monthly plans for 365 or 730-day policies at $100,000 coverage or higher, with a small premium surcharge for the extended term.

For most families, spreading a $2,000-$2,500 annual premium into monthly payments of $165-$210 is far more manageable. It doesn't change the coverage - your parent is fully protected from day one.

Check monthly payment options at DaddySafe.ca →

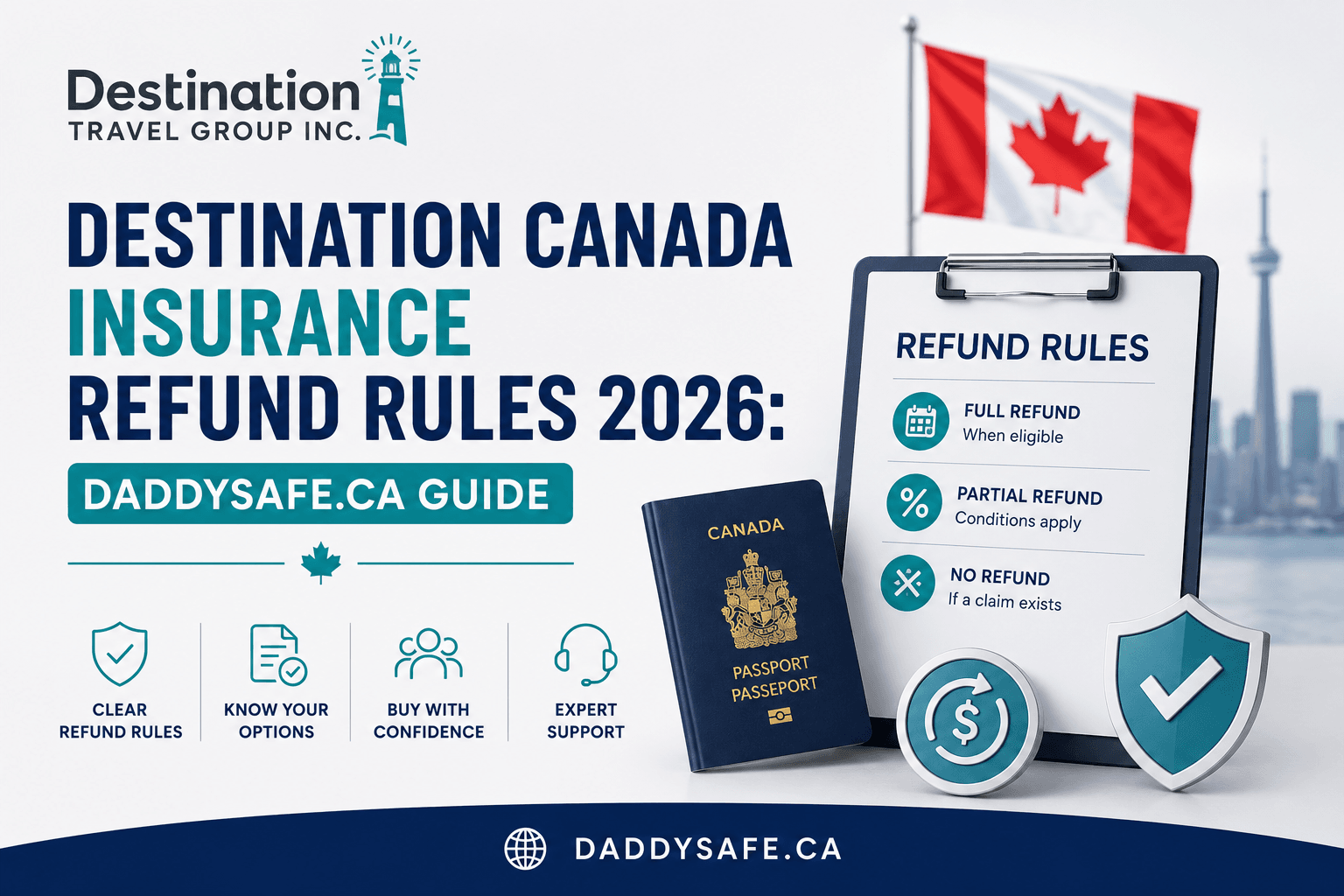

What Happens If the Visa Gets Denied?

You buy the insurance. Then the visa gets denied. What now?

You get your money back. All of it - provided no claim was made and you submit the refund request before the coverage effective date. Every major provider we work with at DaddySafe follows this policy. It's standard across the industry.

Keep the visa denial letter. You'll need it as documentation for the refund request.

Partial refunds are also available if your parent leaves Canada early - before the policy expires - again, provided no claim was filed. Most providers require a minimum premium of around $25 to be retained.

So Which Provider Should You Actually Choose?

Honest answer? It depends.

For a healthy parent under 65 where cost is the priority - RIMI Standard is hard to beat. Lowest premiums in most age brackets, solid coverage for emergencies that aren't pre-existing.

For a parent with managed health conditions - RIMI Enhanced gives you the best value for pre-existing coverage. Significantly cheaper than Manulife Plan B or 21st Century Enhanced for the same protection.

For families who want a well-known name and strong claims support - Manulife and GMS both have excellent reputations, clear policy language, and strong 24/7 assistance infrastructure. You pay a bit more but the peace of mind is real.

For parents aged 70 and above - compare carefully. Premium differences between providers are largest in this bracket. A proper comparison at DaddySafe.ca will show you the real spread before you commit.

Frequently Asked Questions

How much does Super Visa insurance cost in Canada in 2026?

For a parent aged 65-69 with $100,000 coverage, you're looking at roughly $1,621 to $3,259 per year depending on the provider, deductible, and whether pre-existing conditions are covered. Younger parents pay less. Older parents pay more. Compare live quotes at DaddySafe.ca.

What is the minimum Super Visa insurance coverage required?

IRCC requires a minimum of $100,000 CAD from a Canadian provider, valid for at least one year from the date of entry.

Can I pay Super Visa insurance monthly?

Yes. Destination Canada and 21st Century (RIMI) both offer monthly payment plans for $100,000+ coverage on policies of at least 180 days.

Does Super Visa insurance cover pre-existing conditions?

Standard plans do not. Enhanced plans - Manulife Plan B, RIMI Enhanced, 21st Century Enhanced, Destination Canada Option 1 - do cover stable pre-existing conditions, subject to stability periods ranging from 90 to 180 days depending on the provider and your parent's age.

Which is the cheapest Super Visa insurance in Canada?

Based on current rate cards, RIMI Standard is the most affordable in most age groups. But cheapest isn't always right - if your parent has any health conditions, a plan that excludes pre-existing coverage could leave you exposed to a very large uncovered claim.

Can I get a refund if the Super Visa is denied?

Yes - full refund from all major providers if the visa is denied and no claim has been made, submitted before the policy effective date.

One Last Thing

I've been helping families with Super Visa insurance for years. The families who make the best decisions are the ones who take 10 minutes to actually compare - not just pick the first result on Google or go with whatever their cousin recommended.

DaddySafe.ca was built specifically to make that comparison easy. No phone calls. No salespeople. Just live prices from Manulife, GMS, RIMI, Destination Canada, and 21st Century - side by side - in under two minutes.

Compare Super Visa insurance quotes now at DaddySafe.ca →

Sources:

Related Blogs