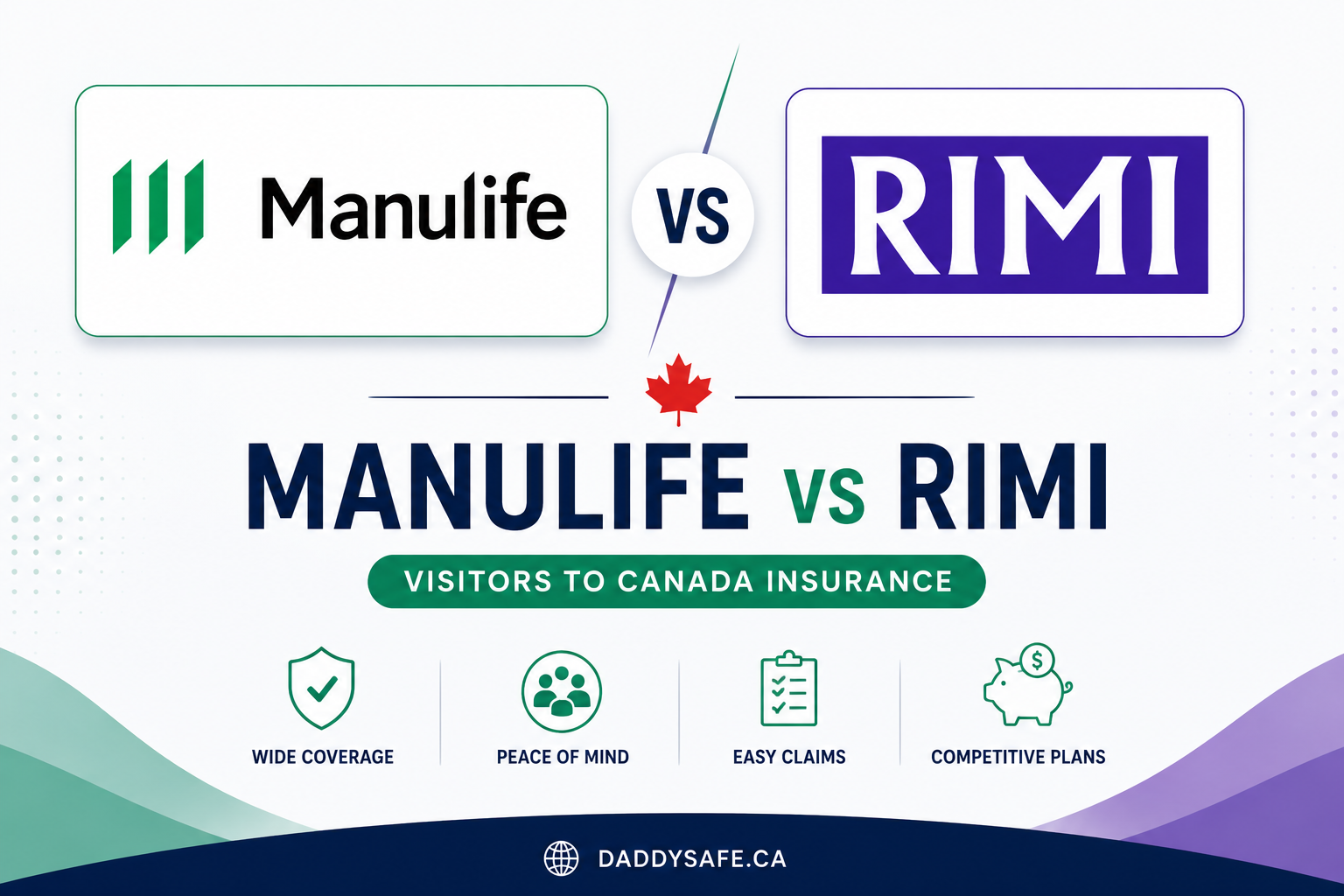

Manulife vs RIMI Super Visa: The Million-Dollar Coverage Question

Three years ago, almost nobody chose $1 million Super Visa coverage. The biggest plans were $300K, and that felt like enough. Then a few high-profile Canadian hospital cases particularly stroke admissions and oncology workups that ran past $200K started making the rounds. Sponsor families started asking for higher tiers. RIMI was the first to offer a $1M plan.

That is why Manulife versus RIMI is one of the most common comparisons we see today. It is essentially a question about how much catastrophic protection a family wants to buy.

Coverage limits the headline difference

Manulife tops out at $300,000. That is enough for the vast majority of Super Visa stays. It is not enough for a major cardiac event with complications, a stroke requiring weeks of rehab, or an oncology workup that involves multiple specialists and imaging.

RIMI goes to $1,000,000. Same underwriting class stable pre-existing covered, 180-day stability but with a coverage ceiling that absorbs almost any realistic medical scenario in Canada.

What you actually pay for the upgrade

For a 70-year-old, healthy, $300K coverage, $1,000 deductible:

Manulife Plan B at $300K: roughly $4,300 to $5,100 per year.

RIMI Standard at $300K: roughly $4,500 to $5,400 per year.

About the same. The real cost difference shows up when you push RIMI toward the higher tiers $500K or $1M which Manulife cannot match.

For the same applicant at RIMI's $1M tier: roughly $5,400 to $6,500 per year. Roughly 25 percent more than the Manulife $300K plan, for more than 3x the coverage limit.

The hospital room conversation

This is the other part most families do not realize until they see the quote. Manulife policies generally pay for ward rooms typically a 3- to 4-bed shared room. RIMI Enhanced upgrades to a semi-private room (2-bed), and also includes meals for an accompanying family member and transport-to-bedside coverage if the visitor ends up hospitalized far from where the host family lives.

For long Super Visa stays where a parent might end up admitted for more than a few days, the comfort difference is real. It is not just about the medical care it is about whether a spouse or adult child can be at the bedside without burning through their own savings on flights and hotels.

Where each one wins

Manulife broadest network, highest age cap (89), strongest answer for parents over 85 since RIMI cuts off at 84. Most budget-friendly for families staying in the $100K to $300K coverage range.

RIMI only path to $500K or $1M coverage. Only insurer offering semi-private rooms and transport-to-bedside. Premium coverage at a surprisingly small uplift over base Manulife.

Our honest take

If you are buying $200K to $300K coverage for a healthy parent under 85, Manulife usually wins on price and network. If you want $500K or more, or you want the comfort upgrades, RIMI is the better answer. Over age 85, only Manulife will write you.

The reason DaddySafe exists is that no single insurer is the right answer for every Canadian family. The platform runs all five at once Manulife, GMS, 21st Century, Destination Canada, RIMI so you can see who wins for your specific parent, age, health, and coverage need.

Compare all 5 Super Visa quotes →

DaddySafe is operated by Immunis Financial Brokers Inc., a licensed Canadian brokerage. The premium ranges referenced here come from real-time 2026 quotes across the comparison platform and shift constantly. Always check the live quote and the actual policy wording before you buy.

Related Blogs